Tax Planning and The Tax Cuts and Jobs Act

The tax year 2018 is quickly ending. The Tax Cuts and Jobs Act (TCJA) makes tax planning more challenging this year, but certainly not impossible. Over the following weeks, we will be discussing various aspects of the TCJA, which must be considered to maximize the tax benefits available to individuals and businesses.

One planning strategy that was enhanced by the TCJA is in the form of Bonus Depreciation and the Section 179 expensing election.

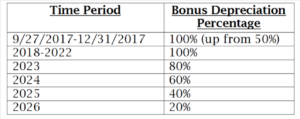

Bonus depreciation allows greater first-year depreciation of property placed in service than the general MACRS or straight-line method of depreciation and is an excellent way to reduce tax liability while investing in your business. Under the TCJA, for assets placed in service in 2018, the definition of qualified assets now includes used property. Previously, used property did not qualify for bonus depreciation. The following chart shows the depreciation percentage for the applicable TCJA period through 2026:

This additional first-year depreciation includes tangible property with a recovery period of 20 years or less (such as office equipment, furniture, and off-the-shelf computer software). However, due to a drafting error in the new law, qualified improvement property (QIP) is no longer eligible for bonus depreciation unless Congress issues a technical correction.

QIP is defined as any improvement to an interior portion of a building that is nonresidential real property if such improvement is placed in service after the date the building was initially placed in service. It does not include any improvement for which the expenditure is used to enlarge the building, add an elevator or escalator, or change the internal structural framework of the building. The U.S. Senate Finance Committee released text of a letter sent to the Treasury and IRS, which identifies issues in the new tax law that require technical corrections. The letter includes QIP as one of these corrections. Please check back on our website for future updates to this law.

Section 179 expensing election allows you to fully deduct qualified property subject to certain limits. This election includes qualified improvement property. Under the TCJA, for qualified property placed in service beginning in 2018, the expensing limit increases to $1 million and begins to phase out dollar for dollar when asset acquisitions for the year exceed $2.5 million. This deduction is limited to offset net income and cannot create a net operating loss.

Please consult with your tax professional to verify that your specific asset purchase qualifies as there are always exceptions to the rule! In our next article, we will discuss the new rules related to itemized deductions on individual tax returns.