Prior to the Tax Cuts and Jobs Act (TCJA), taxpayers could exchange like-kind business property (such as trading in a business vehicle) and defer any gain until the property was ultimately sold. Property that was eligible for this tax-free exchange included both real and personal property. If you traded in a business vehicle in 2017 or earlier, you may not have paid capital gains tax. With the tax laws that passed in 2018, that may no longer be the case, and it’s important to work with a CPA who can ensure you’re handling your trade appropriately on your tax return.

What has changed with the new tax law?

The TCJA has eliminated the deferral of gain or loss on the exchanges of tangible personal property (such as business vehicles) made on or after January 1, 2018. Prior law allowed taxpayers to take 50% bonus depreciation only on new property. Bonus depreciation allows businesses to take a deduction on the purchase of new or used business property or equipment in the year it’s purchased, as opposed to spreading out the deduction over the lifetime of the property in traditional depreciation. The TCJA improved bonus depreciation for business owners by increasing the bonus rate and eliminating the rule that the property had to be new. In 2018, taxpayers can now take 100% bonus depreciation on all qualifying property, whether new or used.

The TCJA also increased the Section 179 limits, which give business owners another option to write off the cost of property purchased. For the 2018 tax year, taxpayers can take an annual deduction of $1 million as long as the total property acquired in the year is under $2.5 million.

To illustrate the change to like-kind exchanges, let’s look at an example.

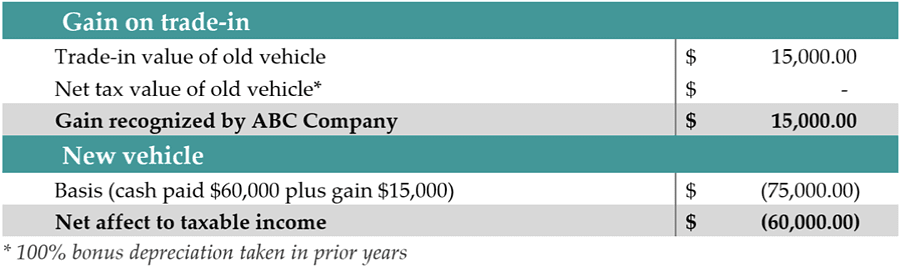

ABC Company needs to replace a vehicle with an original purchase price of $50,000 that was used in its construction/real estate business. The business trades the vehicle against the purchase of the new vehicle. The old vehicle traded in was fully depreciated, with a $15,000 trade-in value. The new vehicle costs $75,000, so ABC pays $60,000 for the new vehicle.

Taxpayers can no longer defer the gain on the disposal of tangible property through a like-kind exchange, which allowed taxpayers to avoid a capital gains tax when replacing an asset, like in the example above. However, the net impact to taxable income has not changed. In the example above, the taxpayer has a $60,000 net deduction against taxable income. Under the old rules, the like-kind exchange would have deferred tax on the $15,000 capital gain and any depreciation recapture on the original property. As of tax year 2018, the business will have to pay tax on the $15,000 capital gain.

What is depreciation recapture?

Depreciation recapture is a tax provision that allows the IRS to collect taxes on any profitable sale of an asset that the taxpayer had used to offset his or her taxable income. Depreciation recapture is assessed when the sale price of an asset exceeds the adjusted cost basis. The difference between these figures is thus recaptured by reporting it as income. Recall our example above: the $50,000 vehicle, which was fully depreciated, had a $15,000 trade-in value.

Since depreciation of an asset reduces ordinary income, a portion of the gain from the disposal of the asset must be reported as ordinary income, rather than the more favorable capital gain. There is no depreciation recapture if a loss was realized on the sale of a depreciated asset. In the example above, the business took 100% of the value of the vehicle in depreciation, which is recaptured when calculating the gain on the sale or trade of the vehicle.

The biggest difference from past years is that this tax cannot be deferred—you need to pay it every time you trade in a vehicle or other piece of business equipment. Every situation is a little bit different, so it’s important to consult with your CPA.

If you have any questions on like-kind exchanges and how they might affect your tax planning strategy, please contact our Jacksonville-based CPA firm to schedule a consultation.